What is a Special Purpose Acquisition Company (SPAC)

and why are they all the current rage for going public?

Special purpose acquisition companies, otherwise known as SPACs, a popular vehicle for privately held businesses to enter the public market has seen a significant amount of activity over the last several months. The U.S. stock market had 480 IPOs in 2020; slightly more than half — 248, in fact — were leveraged by a SPAC. SPAC IPOs in 2020 alone surpassed 2019’s total IPO transactions of 233.

But what exactly are SPACs? Let’s take a look at how these vehicles are used as an alternate route to take a private company public instead of the traditional IPO process, why they are so popular now, and some of the risks and possible pitfalls.

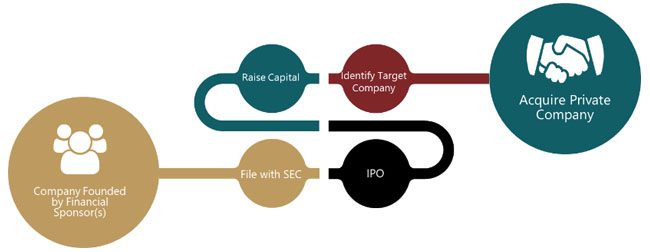

At a high level, a SPAC is shell company funded by financial sponsor(s), in exchange for founders’ stock, typically equating to 20% interest. Once formed, the shell company files with the U.S. Securities and Exchange Commission (SEC) for an IPO and raises additional capital from public shareholders in exchange for units, typically equating to 80% interest, consisting of common stock and warrants. While the shell has a management team, there is usually no operations as the sole objective of the SPAC is to find a private company target to acquire. When a target company is identified, shareholders must approve the transaction. Once acquired, the target company’s operations will then fill the shell and the private company becomes a public company.

So, why use a SPAC instead of the traditional IPO route? Well, a large contributor to the rise in the use of a SPAC IPO is market volatility. Market volatility may change a company’s valuation dramatically during the traditional IPO process. A SPAC IPO allows for less fluctuation in the pricing of the target company. Additionally, venture capital and private equity funds have capital on hand to invest. A SPAC IPO addresses both the market volatility issue and also provides a vehicle that is attractive to venture capital and private equity funds.

However, there are a quite a few challenges involved with SPACs including, but not limited to:

- Regulatory reporting considerations, such as:

- SEC filings,

- Proxy/registration requirements, and

- Super 8-K;

- Various accounting determinations are required such as is the target of an ‘accounting acquirer,’ if it qualifies as an emerging growth company (ECG), or if the transaction is an acquisition or recapitalization;

- Post-transaction Internal Controls over Financial Reporting (ICFR) requirements;

- Timing: The merger needs to occur within 18-24 months. So if the merger does not occur within the specified time frame, the proceeds, which are held in escrow, are returned to the shareholders.

If the first quarter of 2021 is any indication of what the rest of the year looks like it doesn’t appear that the use of SPACs as a vehicle for entering the public markets will be diminishing anytime soon.

The information presented here should not be construed as legal, tax, accounting, or valuation advice. No one should act on such information without appropriate professional advice and after a thorough.